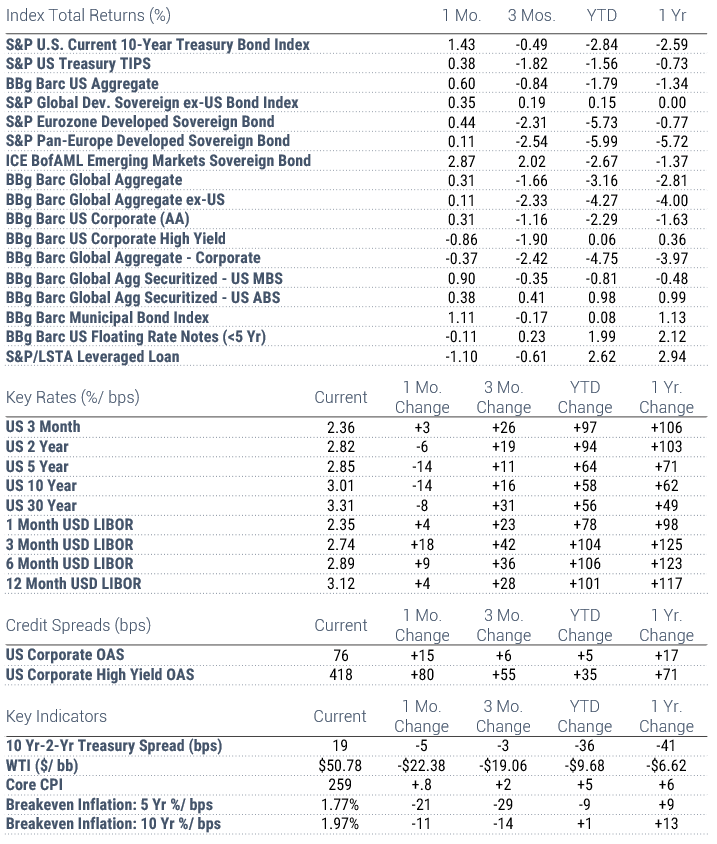

November 2018 Fixed Income Markets Review

After crumbling alongside equities during October’s painful sell-off, fixed income broad-markets offered a strong showing throughout a choppy November. While risk-off sentiment periodically got the better of equities during the month, core US bonds rose steadily, if modestly, amidst that market action and were led higher at month-end by Treasuries as they rallied on dovish comments by Fed Chairman Jay Powell.

Late in the month the US 10-Year yield dipped briefly below 3% before closing out at 3.01%; a retreat in yields pushed prices higher, and the US Current 10-Year Treasury Bond Index led US markets with a gain of 1.43%. The US Aggregate Bond Index gained 60 basis points versus a Global Aggregate Bond Index that added 31 basis points (local currency). US investment-grade corporates (+0.31%) rebounded partially off of October’s losses but weren’t enough to offset losses in ex-US credit and the global corporate index overall shed around 40 basis points. US high yield continued to struggle, falling nearly 90 basis and all but erasing year-to-date performance.

The S&P Eurozone Developed Sovereign Bond Index added 44 basis points, rallying alongside US treasuries and as core inflation fell alongside oil prices and industrial production – factors that, in aggregate, may stall tightening by European central banks. German yields sank as Italian bond prices stabilized versus the prior month (during which Moody’s downgraded the country’s debt to just one notch above investment-grade). Results were mixed outside the Eurozone.

Emerging market debt prices rose steadily throughout the month and sharply in response to comments by the Fed Chairman, with investors calculating that a halt in US rate-hikes may serve to defer global portfolio rebalancing away from higher-risk issuers and soften the dollar in the process. Yields on Chinese and Indian 10-year bonds fell roughly the same amount as the US 10-year, and the sovereign index rose 2.47%.

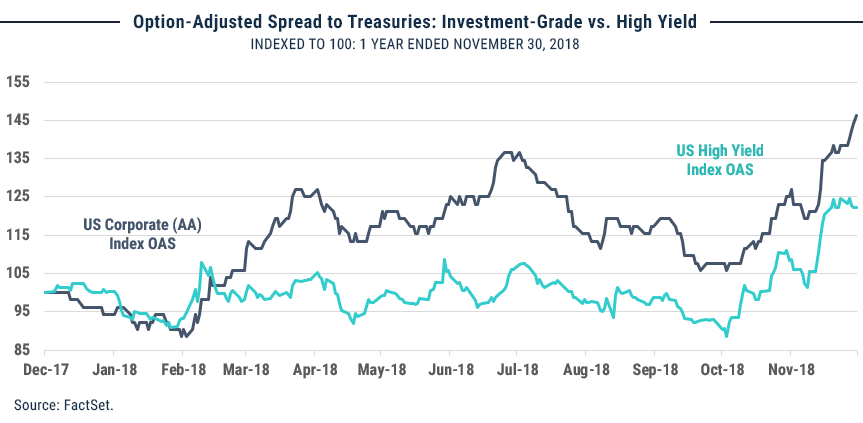

Spotlight: Credit

Just a handful of sectors remain in the black year-to-date but a sudden surge in credit market volatility has worked to erode gains in riskier segments such as high yield and leveraged loans – high yield, for example, in October posted its worst monthly return since 2015 and saw spreads widen another 80 basis points in November. Investment-grade credit spreads have widened as well and as the chart below shows, at an even faster clip year-to-date. While core bond investors were happy to focus on Chairman Powell’s “just below (neutral level)” comment with respect to rates, it seems that credit investors may have tuned into Fed concerns about credit quality against the fast-growing ratio of corporate debt to GDP.

For more market reviews, visit the WST blog.

For more market reviews, visit the WST blog.

Index Returns – all shown in US dollars

All returns shown trailing 11/30/2018 for the period indicated. “YTD” refers to the total return as of prior-year end, while the other returns are annualized. 3-month and annualized returns are shown for:

- The Barclay’s US Aggregate Index, a broad based unmanaged bond index that is generally considered to be representative of the performance of the investment grade, US dollar-denominated, fixed-rate taxable bond market.

- The ICE BofAML Emerging Markets Sovereign Bond Index is a subset of The BofA Merrill Lynch World Sovereign Bond Index excluding all securities with a country of risk that is a member of the FX G10, all Western European countries, and territories of the U.S. and Western European countries. The FX G10 includes all Euro members, the U.S., Japan, the U.K., Canada, Australia, New Zealand, Switzerland, Norway, and Sweden.

- The Bloomberg Barclays Global Aggregate Index, which measures global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers.

- The S&P Global Developed Sovereign Bond index includes local-currency denominated debt publicly issued by governments in their domestic markets.

- S&P Eurozone Developed Sovereign Bond - seeks to measure the performance of Eurozone government bonds.

- The S&P Pan-Europe Developed Sovereign Bond Index is a comprehensive, market-value-weighted index designed to track the performance of local currency-denominated securities publicly issued by Denmark, Norway, Sweden, Switzerland, the U.K. and developed countries in the Eurozone for their domestic markets.

- ICE BofAML Emerging Markets Sovereign Bond - tracks the performance of US dollar (USD) and Euro denominated emerging markets non-sovereign debt publicly issued within the major domestic and Eurobond markets.

- The Bloomberg Barclay’s US Corporate Bond Index (AA), which measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD denominated securities publicly issued by US and non-US industrial, utility and financial issuers.

- The Bloomberg Barclay’s US Corporate High Yield Index, which covers the USD-denominated, non-investment grade, fixed-rate, taxable corporate bond market.

- Bloomberg Barclay’s Global Aggregate Securitized- US Mortgage-Backed Securities, which is a component of the Bloomberg Barclay’s US Aggregate Index and measures investment grade mortgage backed pass-through securities of GNMA, FNMA, and FHLMC.

- Bloomberg Barclay’s Global Aggregate Securitized- US Asset-Backed Securities, which is a component of the Bloomberg Barclay’s US Aggregate Index and includes the pass-throughs, bullets, and controlled amortization structures of only the senior class of ABS issues.

- The Blomberg Barclay’s US Floating Rate Notes (<5 Yr) Index, measures the performance of U.S dollar-dominated, investment grade floating rate notes with maturities less than 5 years.

- The Bloomberg Barclay’s Municipal Bond Index, which measures investment grade, tax-exempt bonds with a maturity of at least one year.

- The S&P/ LSTA Leveraged Loan Index is designed to reflect the performance of the largest facilities in the leveraged loan market.

Key Rates

Key Rates are shown for US Treasurys and London Interbank Offered Rate (LIBOR), the interest rate at which banks offer to lend funds (wholesale money) to one another in the international interbank market. LIBOR is a key benchmark rate that reflects how much it costs banks to borrow from each other. “Current” refers to the percentage rate as of 6/30/2018, while the rates of change are stated in basis points.

Credit Spreads

Credit Spreads shown comprise the Option-Adjusted Spread of the indices indicated, versus the US 10-Year Treasury Yield. “Current” refers to the spread as of 6/30/2018, while the rates of change are stated in basis points.

Key Indicators

Key Indicators correspond to various macro-economic and rate-related data points that we consider impactful to fixed income markets.

- 2s10s (bps)/ 10 Yr vs 2 Yr Treasury Spread, which measures the difference between yields on 10-Year Treasury Constant Maturity Securities and 2-Year Treasury Constant Maturity Securities.

- West Texas Intermediate, which is an oil benchmark and the underlying asset in the New York Mercantile Exchange’s oil futures contract.

- Core Consumer Price Index, which measures the consumer price index excluding food and energy prices. Shown as of the prior month-end.

- Breakeven Inflation: 5 Yr %/ bps, which uses 5-Year Treasury Constant Maturity Securities and 5-Year Treasury Inflation–Indexed Constant Maturity Securities to derive expected inflation.

- Breakeven Inflation: 10 Yr %/ bps, which uses 10-Year Treasury Constant Maturity Securities and 10-Year Treasury Inflation–Indexed Constant Maturity Securities to derive expected inflation.

General Disclosure

This document is intended for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product. This material is proprietary and being provided on a confidential basis, and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein includes information that has been obtained from third party sources and has not been independently verified. It is made available on an "as is" basis without warranty and does not represent the performance of any specific investment strategy.

This material is proprietary and being provided on a confidential basis, and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein includes information that has been obtained from third party sources and has not been independently verified. It is made available on an "as is" basis without warranty and does not represent the performance of any specific investment .Some of the information enclosed may represent opinions of WST and are subject to change from time to time and do not constitute a recommendation to purchase and sale any security nor to engage in any particular investment strategy. The information contained herein has been obtained from sources believed to be reliable but cannot be guaranteed for accuracy. Past performance is not necessarily indicative of future results. Securities and services are not FDIC or any other government agency insured – Are not bank guaranteed – May lose Value.

Besides attributed information, this material is proprietary and may not be reproduced, transferred or distributed in any form without prior written permission from WST. WST reserves the right at any time and without notice to change, amend, or cease publication of the information. This material has been prepared solely for informative purposes. The information contained herein may include information that has been obtained from third party sources and has not been independently verified. It is made available on an “as is” basis without warranty. This document is intended for clients for informational purposes only and should not be otherwise disseminated to other third parties. Past performance or results should not be taken as an indication or guarantee of future performance or results, and no representation or warranty, express or implied is made regarding future performance or results. This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security, future or other financial instrument or product.